By Joe Quinn

Aluminum is one of the foundational industrial materials of modern society, integral to everything from passenger airplanes to kitchen appliances. Recent U.S. legislative incentives – lead by the Inflation Reduction Act (IRA) – to produce more solar panels, EVs, electrical charging infrastructure, and other clean energy transition products will increase the demand for primary aluminum only further. However, as a recent SAFE report shows, the series of bills do not address the main obstacle to producing primary aluminum within the United States: access to ample supplies of affordable energy.

Unlike other critical minerals necessary for the clean energy transition, primary aluminum has a long history of processing and manufacturing in the U.S. Yet, in the last two decades, U.S. primary production fell from first to ninth globally. Furthermore, the world’s top producer, China, now generates 45 times more primary aluminum than the United States. While the United States is not overly reliant on primary processed in China (currently imports of all types of Chinese aluminum sit around six percent), China’s overproduction of primary suppresses the global price for aluminum, making it more difficult for domestic smelters to compete—and therefore, effectively undercutting downstream and secondary aluminum production in the United States. Less domestic production across segments increases supply chain inefficiencies, as the U.S. market benefits from having the largest customer market at home.

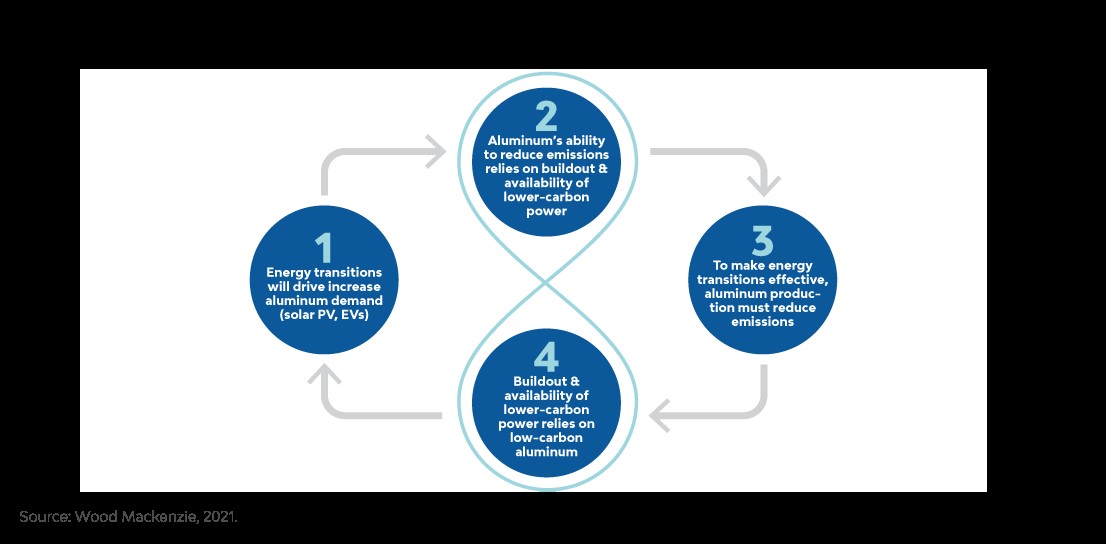

Underlying the geopolitical hurdle of Chinese market distortion, the root of the primary challenge at home is energy. Primary aluminum needs stable, abundant, and affordable sources of electricity to ensure smelter viability and economic competitiveness. Countries with ample and cheap energy, like Iceland, Canada, the UAE, and Russia have been able to sustain and even grow primary production in the face of Chinese market flooding. The shift to renewable energy sources, which is accelerating demand for aluminum, can be a solution for domestic smelters—if the right policies are in place.

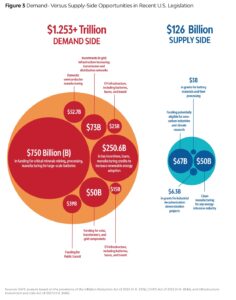

Recent U.S. attempts at these policies include the 2022 Inflation Reduction Act, the 2021 Infrastructure Investment and Jobs Act, the Defense Production Act, and the 2022 CHIPs Act, all of which cumulatively increase demand for aluminum in significant ways:

• The IRA incentivizes more production of solar polar, batteries, and electric vehicles, the latter requiring hundreds of pounds more aluminum (per automobile) compared to traditional internal combustion engine vehicles.

• The IIJA funds $73B for aluminum-heavy electric infrastructure and $5B for a nationwide network of EV charging stations.

• DPA supports the domestic production of strategic materials, including aluminum, used in large-capacity batteries used in EVs and military systems.

• CHIPS Act sets aside $39 billion in direct federal assistance to produce semiconductors in the US, which is the fastest growing demand share of high purity aluminum discs.

These laws do offer some supply-side support, specifically the vitally important manufacturing production tax credit (45X) and investment tax credit (48c). However, the support they provide is contingent on decarbonization and funding is highly competitive.

The domestic industry is entangled in a clean energy paradox where it cannot deliver on new demand for aluminum use such as solar panels, EVs, and grid as it struggles to stay afloat due to the volatile cost of electricity for aluminum production.

Additional interventions to connect U.S. aluminum production to these new energy sources are needed. Reliable, affordable, and abundant sources of cleaner electricity sources will release domestic smelting from the energy trap – and provide the material needed to build out America’s overdue energy transition.

Joe Quinn is a Vice President at SAFE and the Director of the Center for Strategic Industrial Materials. He is former Vice President of External Affairs and Industry Relations for the Aluminum Association.

More from Joe on this topic:

The US Aluminum Production Challenge and How to Fix It – Force Distance Times

A Chance to Revive and Decarbonize American Manufacturing — RealClearEnergy